Presenter(s)

Sallie Rebecca DeYoung

Files

Download Project (539 KB)

Description

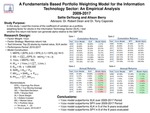

A central proposition in finance theory is that investors are risk averse and attempt to minimize the risk relative to expected returns regardless of the particular asset class being considered as an investment. In this study, I combine a fundamentals-based approach to portfolio weighting with a measure of return relative to risk to generate portfolio performance for the Top 20 Stocks by market value in the SPDR Information Technology Sector. I use a three-year moving average of each stock’s earnings per share to calculate the inverse of the coefficient of variation (1/cov), a return-risk ratio. Higher portfolio weights are given to stocks with higher 1/cov ratios. Stock weights are recalculated each year so that the portfolio is rebalanced annually. The initial investment is $1,000,000. Portfolio returns are generated for the years 2009-2017 and the performance benchmark is the SPDR S&P 500 ETF (SPY).

Publication Date

4-18-2018

Project Designation

Independent Research

Primary Advisor

Tony S. Caporale, Robert D. Dean

Primary Advisor's Department

Economics and Finance

Keywords

Stander Symposium project

Recommended Citation

"A Fundamentals Based Portfolio Weighting Model for the Information Technology Sector:An Empirical Analysis: 2009-2017" (2018). Stander Symposium Projects. 1129.

https://ecommons.udayton.edu/stander_posters/1129