Presenter(s)

Sarah Claiborne, Sean Dee

Files

Download Project (917 KB)

Description

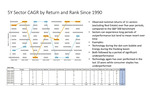

For our project, we calculated the single year return for each of the sectors of the S&P 500 (excluding real estate) since January 1, 1990. After calculating the single year return, we created a table to visualize returns compared to the benchmark. In this table, we can observe how industries returned nominally when directly related to the S&P 500. This table reaffirms our findings in the 5-year period as each sector can have multiple years of either over or underperforming the index. This allows us to conclude that performance in a single year does not necessarily drive a mean reverting tendency in a one-year period but may possess a mean reverting tendency over a longer time frame. The next step in confirming this would be creating a regression that lags the performance of each sector. This can help us determine with statistical confidence over various time periods. In the short-term momentum appears to be a determinate of results, but potentially shifting as the time gets stretched longer.

Publication Date

4-23-2025

Project Designation

Independent Research

Primary Advisor

Henry G. Willmore

Primary Advisor's Department

Economics and Finance

Keywords

Stander Symposium, School of Business Administration

Recommended Citation

"5Y Sector CAGR by Return and Rank since 1990" (2025). Stander Symposium Projects. 4150.

https://ecommons.udayton.edu/stander_posters/4150

Comments

9:00-10:15, Kennedy Union Ballroom