Presenter(s)

Tyler B Cronin, Leah M Haverkos

Files

Download Project (236 KB)

Description

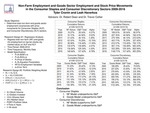

Employment growth is considered a key measure of macroeconomic activity. Rational expectation theory, therefore, would expect a positive linkage between employment growth and the price movement of common stocks. In this study, we examine the relationship between non-farm employment and the goods sector employment growth and price movements in Consumer Staples (XLP) and Consumer Discretionary (XLY) stocks. Using regression analysis, we regress employment growth on the top ten stocks in each of the above sectors (i.e. XLP and XLY). We test the hypothesis that the B coefficients in the regressions are > 0 and statistically significant at the 95% confidence level (T>2).

Publication Date

4-5-2017

Project Designation

Independent Research - Undergraduate

Primary Advisor

Trevor C. Collier

Primary Advisor's Department

Economics and Finance

Keywords

Stander Symposium project

Recommended Citation

"Marco Economic Activity And Stock Price Movements: A Closer Look At The Covariation Between Total Non-Farm Employment Plus Goods Sector Employment And S&P 500 Stock Prices, 2009-2016." (2017). Stander Symposium Projects. 851.

https://ecommons.udayton.edu/stander_posters/851