Presenter(s)

William Binnie

Files

Download Project (153 KB)

Description

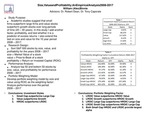

In this study I extend the analysis of Fama and French and Novy-Marx on the effect of firm size, value and profitability on a portfolio's excess returns. The period analysis is 2008 -2017. For this analysis I use the same metrics for size (market value) and value (price to book) as Fama and French but differ in my measure of profitability. I use return on invested capital (ROIC) instead of return on equity or gross operating profits as a percent of assets because ROIC is considered a better measure of measure of the efficient allocation of capital as well as the firm's ability to generate economic value added. I test the following hypothesis. 1.) High ROIC large cap stocks outperform low ROIC large cap stocks 2.) High ROIC small cap stocks outperform low ROIC small cap stocks 3.) High ROIC value stocks outperform low ROIC value stocks 4.) High ROIC growth stocks outperform low ROIC growth stocks

Publication Date

4-18-2018

Project Designation

Independent Research

Primary Advisor

Tony S. Caporale, Robert D. Dean

Primary Advisor's Department

Economics and Finance

Keywords

Stander Symposium project

Recommended Citation

"Size, Value, and Profitability in the Cross Section of Returns: An Empirical Analysis, 2008 - 2017." (2018). Stander Symposium Projects. 1143.

https://ecommons.udayton.edu/stander_posters/1143