Presenter(s)

Thomas L. Goslee, Nathan Glenn Jabaay, Thomas Charles Letke

Files

Download Project (117 KB)

Description

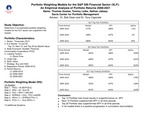

In this study we develop concentrated portfolios of ten and twenty stocks for theS&P 500 Financial Sector ETF (XLF). We use a factor mimicking regression model to determinethe portfolio weights for each stock. We regress the "state" economic variable Consumer Spendingon Revenue Per Share(the factor loading) and use the slope coefficients as our factor weights.Portfolio returns are calculated for the periods 2009-2019,2009-2020,and 2009-2021. We test the hypothesis that Consumer Spending is a latent priced-in risk factor throughits effect on Revenue Per Share growth i.e., our portfolio weighting models outperform thebroad market. The addition of the cumulative return periods 2009-2020 and 2009-2021 alsoallows us to determine if Covid-19 and rising interest rates had an impact on portfolio returns.

Publication Date

4-20-2022

Project Designation

Independent Research

Primary Advisor

Tony S. Caporale, Robert D. Dean

Primary Advisor's Department

Economics and Finance

Keywords

Stander Symposium project, School of Business Administration

United Nations Sustainable Development Goals

Quality Education

Recommended Citation

"Concentrated Portfolios, Profitability and the S&P 500 Financial Sector: An Empirical Analysis of Long Run Returns, 2009-2021." (2022). Stander Symposium Projects. 2666.

https://ecommons.udayton.edu/stander_posters/2666

Comments

Presentation: 9:00 a.m.-10:15 a.m., Kennedy Union Ballroom