Presenter(s)

Hayden Gray, Andrew Kohnen

Files

Download Project (74 KB)

Description

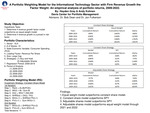

In this study I run two types of portfolio return tests: (1) Determine if the returns for my revenue growth factor weighted portfolio are greater than an equal weight portfolio, 2009-2022. (2) Determine if the revenue growth factor weighted portfolio generates long term excess returns over the broad market index S&P 500 i.e. revenue growth is a priced-in risk factor. I use a buy and hold and an adjustable shares investment strategy to develop portfolio returns for the period 2009-2022.

Publication Date

4-19-2023

Project Designation

Independent Research

Primary Advisor

Jon Fulkerson, Robert Dean

Primary Advisor's Department

Economics and Finance

Keywords

Stander Symposium, School of Business Administration

Institutional Learning Goals

Scholarship

Recommended Citation

"A Portfolio Weighting Model for the Information Technology Sector with Firm Revenue Growth the Factor Weight: An Empirical Analysis of Portfolio Returns, 2009-2022" (2023). Stander Symposium Projects. 2847.

https://ecommons.udayton.edu/stander_posters/2847

Comments

Presentation: 9:00-10:15 a.m., Kennedy Union Ballroom