Presenter(s)

John P. Klinger

Files

Download Project (329 KB)

Description

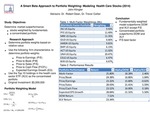

A key factor in portfolio returns is the weights given to stocks in a portfolio of stocks. Capital Asset Pricing Models indicate that the weight assigned to a stock should be based on its risk premium to the market. In recent years, attention has focused on firm size, relative valuation, and earnings momentum as the appropriate weighting strategies. In this study I focus my attention on large size firms in the health care sector using a concentrated portfolio of the 10 largest holdings in the SPDR Health Care ETF. I use a combination of relative value and momentum weighting strategies to develop portfolio weights for the 10 health care stocks. The performance of the concentrated portfolio is compared to the performance of the SPDR Health Care ETF, the DOW, and the S&P 500 for 2014. Quarterly and annual performance comparisons are made assuming that the concentrated portfolio starts 2014 with a funding level of $5,000,000.

Publication Date

4-9-2015

Project Designation

Independent Research

Primary Advisor

Trevor C. Collier

Primary Advisor's Department

Economics and Finance

Keywords

Stander Symposium project

Disciplines

Arts and Humanities | Business | Education | Engineering | Life Sciences | Medicine and Health Sciences | Physical Sciences and Mathematics | Social and Behavioral Sciences

Recommended Citation

"Relative Value and Momentum Weighting for a Concentrated Portfolio of Health Care Stocks" (2015). Stander Symposium Projects. 621.

https://ecommons.udayton.edu/stander_posters/621

Included in

Arts and Humanities Commons, Business Commons, Education Commons, Engineering Commons, Life Sciences Commons, Medicine and Health Sciences Commons, Physical Sciences and Mathematics Commons, Social and Behavioral Sciences Commons